What is an Education Loan? Complete Guide for Students in Nepal

For many Nepali students, the dream of higher education, especially studying abroad, often collides with one major challenge: financial limitations. Rising international tuition fees, visa-related costs, and living expenses make overseas education seem out of reach, even for deserving students with strong academic potential. This financial burden leaves many families unsure of how to move forward.

This is where an education loan plays a crucial role. Whether you are planning to study in Nepal or aiming for universities in countries like Australia, the UK, Canada, or the USA, an education loan helps turn academic ambitions into reality. Understanding how education loans work in Nepal is essential before taking this step.

In this guide, you will learn what an education loan is, how to get one in Nepal, interest rates, and smart repayment tips so you can confidently plan your education journey.

In this blog

What is an Education Loan?

An education loan is financial assistance provided by banks or financial institutions to help students cover the cost of higher education. It is designed to make education more accessible, especially when tuition fees, living expenses, and other study-related costs are beyond what a family can afford. Education loans are not limited to local studies; they are increasingly used by Nepali students who wish to pursue higher education abroad.

Education loans typically cover a wide range of expenses, including:

- Tuition fees for universities and colleges in Nepal or abroad

- Living and accommodation costs while studying in another country

- Travel and visa expenses for overseas education

- Books, research materials, and equipment required for academic programs

- Insurance and other miscellaneous fees

For students planning to study abroad, an education loan can be a practical solution to overcome financial barriers. Banks in Nepal offer specific loans for international education, often requiring a co-applicant, collateral, or proof of admission from the chosen university.

Education loans usually come with flexible repayment options, allowing students to start repayment after completing their course or during a grace period. Interest rates may vary depending on the bank, type of loan, and collateral provided.

Taking an education loan not only helps manage financial stress but also enables students to focus on their studies and career goals without compromise. For aspiring Nepali students, understanding how these loans work, the eligibility criteria, and the application process is essential to make informed decisions for a successful academic journey abroad.

Why Do Students Need an Education Loan in Nepal?

Students looking to study abroad from Nepal often need an education loan to afford higher education without compromising on quality or opportunities. By bridging the gap between financial limitations and educational aspirations, these loans allow students to focus on learning, explore global programs, and preserve family savings for the future. With flexible repayment options and moratorium periods, education loans make both local and overseas studies more accessible and manageable.

1. High Costs of Quality Education

The cost of quality education, whether in Nepal or abroad, can be higher. Tuition fees for reputed institutions are often high, and additional expenses like accommodation, books, and travel add up quickly. For students aspiring to study abroad, these costs can be even higher due to currency exchange, visa, and living expenses. Education loans provide the necessary financial support so that deserving students can pursue top-tier programs without being limited by cost.

2. Financial Accessibility

Not all families can pay for higher education upfront. Education loans create financial accessibility, ensuring that talented students are not left behind due to a lack of funds. This allows students to access a wider range of universities, both within Nepal and internationally, based on merit rather than budget constraints.

3. Preserving Family Savings

Paying for higher education from family savings can put a significant strain on household finances. By taking an education loan, families can avoid depleting their savings while still supporting their child’s academic ambitions. This ensures long-term financial stability for both the student and the family.

4. Flexibility & Moratoriums

Many education loans offer flexible repayment options, including moratorium periods where repayment starts after course completion. This gives students time to settle into their careers and manage finances without immediate pressure. Banks often allow partial prepayment and adjustments in installments, making it easier to handle repayments smoothly.

5. Enabling Study Abroad

For Nepali students aiming to study in Australia, the UK, Canada, or the USA, education loans are often essential. They cover tuition, living, and travel costs that would otherwise be difficult to manage. Without loans, many students would have to limit their choice of programs or countries.

6. Program Choice

Education loans empower students to choose programs based on interest and career prospects rather than affordability. This allows them to pursue specialized courses abroad or advanced programs in Nepal that may significantly improve their career opportunities.

Education Loan Interest Rate in Nepal

Understanding education loan interest rates is essential before you apply for financing, especially if you are planning to study abroad, where costs are significantly higher. In Nepal, interest rates on education loans can vary widely depending on the bank and the type of loan you choose. Most commercial banks offer education loans within a broad range, generally around 5% to 12% per annum, though exact rates change frequently and depend on specific bank policies and agreements with the borrower.

Overview of Current Education Loan Interest Rates

Interest rates on education loans in Nepal are influenced by market conditions and banking regulations. For example, some banks list their education loan rate close to 9.99% to 11.99% for fixed-rate loans, depending on the tenure and loan size. Other banks may offer slightly lower rates or floating options tied to base rate movements.

For students planning to go abroad, these rates are an important consideration because the total cost of the loan (including interest) can be significantly higher due to larger loan amounts and longer repayment tenures. Education loans often come with options for moratorium periods (a pause on repayments until after the study period), but interest still accumulates during that time.

Factors Affecting Interest Rates

Several factors influence how much interest you pay on an education loan:

- Bank policies: Each bank sets its own rates based on risk assessment, market competition, and internal lending strategies.

- Collateral: Loans backed by collateral, like property, may attract lower rates than unsecured loans.

- Study destination: Loans for overseas education sometimes have different terms because the total loan amounts and risk profiles vary.

- Course and duration: Longer courses and professional programs may lead to different rate structures.

Which Bank Has the Lowest Education Loan Interest in Nepal?

Public sector banks like Krishi Bikas Bank and Rastriya Banijya Bank (RBB) have the lowest education loan interest in Nepal. Krishi Bikas Bank offers an education loan at only 5.19% - 7.19% per annum, while RBB offers at 5.42% - 6.42%. Similarly, other banks like Siddhartha Bank and Citizens Bank also offers a competitive fixed rates with added flexibility.

Instead of focusing on a single rate number, compare offers from multiple banks based on:

- Overall interest (fixed vs floating)

- Loan tenure and repayment flexibility

- Processing fees and hidden charges

- Moratorium benefits

This broader approach helps you choose a loan that fits your needs rather than just chasing the lowest percentage.

Importance of Consulting Banks and Education Consultants

Interest rates and loan terms can be complex, especially for study abroad plans where repayments and currency differences matter. Consulting directly with banks and experienced education consultants helps you:

- Get updated interest rate offers based on your specific loan amount

- Understand hidden costs or processing fees

- Choose the best bank based on your goals and repayment capacity

Working with a knowledgeable education consultancy ensures you make informed decisions and get the most suitable loan structure for your academic journey abroad.

How to Calculate Education Loan Interest?

Education loan interest in Nepal can be calculated using either a flat rate or a reducing balance method, and understanding these helps you plan repayments and total cost effectively. Calculating the interest on an education loan is essential for budgeting, especially if you are planning to study abroad. Nepali banks generally use two main methods: flat rate interest and reducing balance interest.

1. Flat Rate Interest Method

In the flat rate system, interest is calculated on the original loan amount for the entire loan period. This method is simpler to compute, but it can result in a higher overall interest cost because the principal amount does not reduce as you make repayments.

Example:

Suppose you borrow NPR 1,000,000 at a flat interest rate of 10% per annum for 4 years.

Total interest = Principal × Rate × Time

= 1,000,000 × 0.10 × 4

= NPR 400,000

So over 4 years, you would pay NPR 400,000 in interest in addition to repaying the principal. The interest amount stays the same each year under this method.

2. Reducing Balance Interest Method

In the reducing balance method, interest is calculated on the outstanding principal amount after each repayment. This means your interest portion decreases over time as your outstanding loan balance reduces.

Example:

If you borrow NPR 1,000,000 at 10% reducing balance interest over 4 years, you pay interest only on the remaining balance each year. Early in the loan term, the interest portion of your payment is higher, but it gradually declines as you repay the principal. Over time, this method generally results in lower total interest paid compared to flat-rate loans.

3. EMI Calculation

Most education loans are repaid through Equated Monthly Installments (EMIs), which combine interest and principal repayment into a single monthly payment. Banks use formulas (or loan calculators) to determine your EMI based on the loan amount, rate, and tenure.

Understanding how your interest is calculated enables you to compare loan options, choose the most cost-effective one, and plan your study abroad expenses with greater confidence.

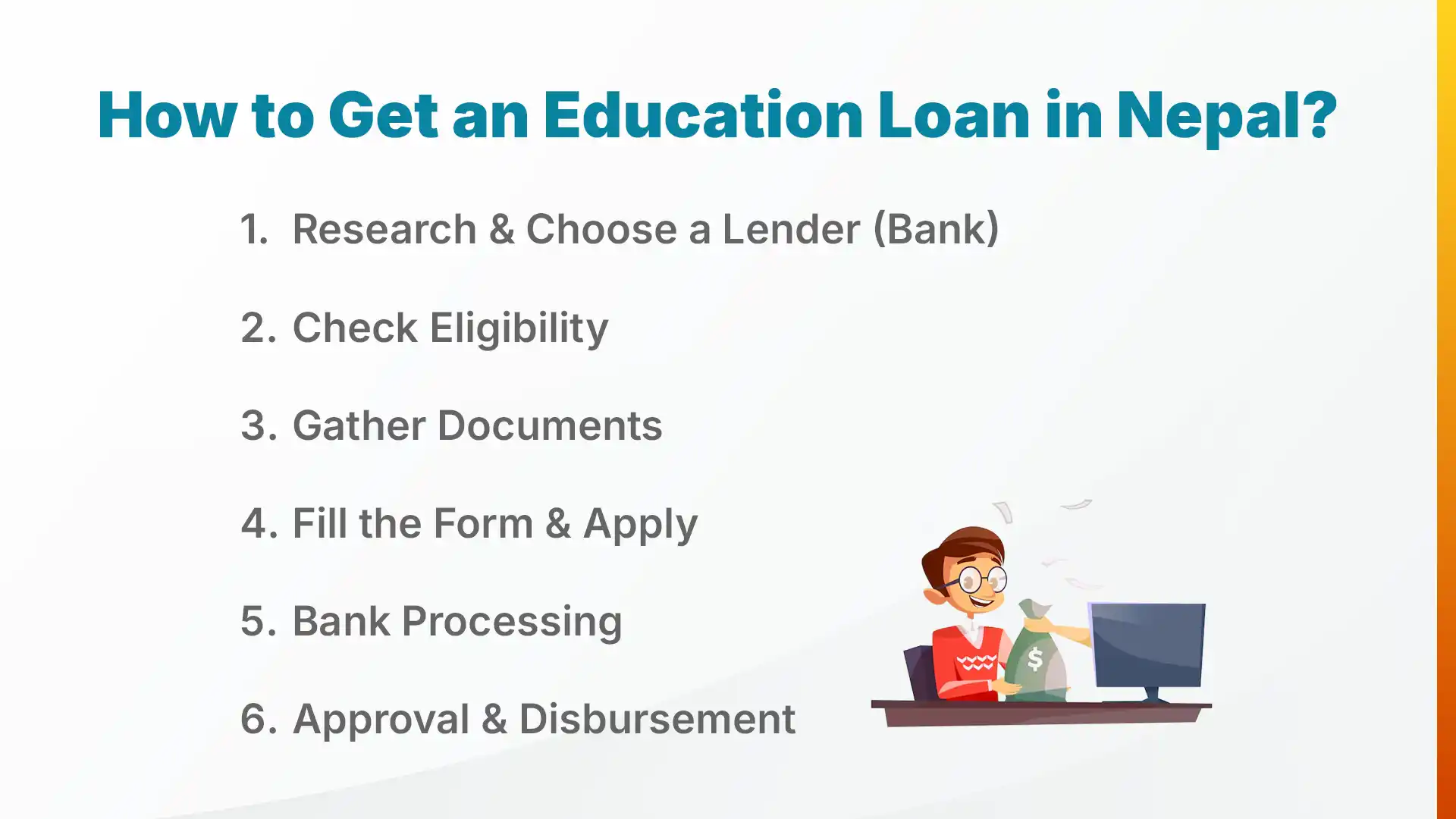

How to Get an Education Loan in Nepal?

To get an education loan in Nepal, choose the right bank, check eligibility, submit the required documents, and complete the bank’s application process. Following these steps carefully ensures smooth approval and timely disbursement, making it easier to fund studies in Nepal or abroad. With proper guidance, students can focus on their academic goals without financial stress.

1. Research & Choose a Lender (Bank)

The first step is to identify banks that offer education loans suitable for your needs. Consider interest rates, repayment options, processing fees, and flexibility for studying abroad. Some banks may provide special schemes for overseas education, while others may have lower rates for local courses. Comparing multiple banks helps you find the most cost-effective and convenient option.

2. Check Eligibility

Before applying, ensure you meet the bank’s eligibility criteria. Most banks require the student to have secured admission to a recognized program, be within a certain age limit, and have a co-applicant (usually a parent or guardian). Eligibility may vary for local versus international education loans, so clarify the bank’s requirements in advance.

3. Gather Documents

Prepare all necessary documents, including admission letters, academic transcripts, identity proof, co-applicant’s financial statements, and collateral papers if required. For studying abroad, you may also need a valid passport, visa, and cost estimates from the foreign institution. Organized documentation speeds up the approval process.

4. Fill the Form & Apply

Complete the bank’s education loan application form accurately. Include all personal, academic, and financial details. Double-check for errors, as incomplete or incorrect forms can delay processing. Submit the application along with all supporting documents to the bank.

5. Bank Processing

After submission, the bank will review your application, verify documents, and assess your repayment capacity. This may include background checks on the co-applicant and evaluation of collateral if needed. The processing period can vary from a few days to a few weeks.

6. Approval & Disbursement

Once approved, the bank issues a sanction letter detailing the loan amount, interest rate, and repayment terms. The loan amount is then disbursed directly to your educational institution, either in full or in installments, depending on the agreement. With the loan in place, you can focus on your studies without worrying about finances.

Documents Required for Education Loan in Nepal

Getting an education loan in Nepal requires a few important documents from both the student and the parent or guarantor. These documents help the bank verify your identity, admission, finances, and collateral if needed. The requirements may vary slightly depending on the bank, but most banks ask for the same basic set. Having all your documents ready makes the loan process faster and smoother.

1. Student Documents

- Application Form: Fill it carefully with all your details.

- Admission: Provide your admission letter or I-20 from the university, course enrollment letter, and visa if you are going abroad.

- Academics: Include all mark sheets and transcripts from SLC/equivalent, +2, and bachelor’s or higher studies.

- Identification: Citizenship certificate and passport if studying abroad.

- Photos: Recent passport-size photos of you and your parents/guarantors.

- Tests: English language test scores, like IELTS or PTE, if required by your university.

2. Guarantor/Parent Documents

- Identification: Citizenship, passport, and relationship certificate (or marriage certificate if applicable).

- Income Proof: Salary certificate for employed parents, or audited financials, rental income, or pension documents if applicable.

- Financials: Bank statements of the last 6 months, tax clearance certificates, and PAN card.

- Assets: Property or business documents to show net worth if required.

3. Collateral Documents (for secured loans)

- Property Papers: Land ownership certificate (Lalpurja), tax receipts, building approval documents.

- Other Security: Fixed deposits or other pledged assets if the bank asks.

4. Other Documents

- NOC: No Objection Certificate from the Ministry of Education (if required).

- Location Map: Maps of residence or office for verification.

Always check with your bank, like Nabil, NIC Asia, Siddhartha, NMB, or Kumari, because requirements can vary slightly. Having everything ready helps you get the loan faster and start your studies without delays.

Eligibility Criteria for Education Loan

To get an education loan in Nepal, both the student and a co-applicant (usually a parent or guardian) must meet certain basic requirements. These rules help the bank make sure the loan can be repaid and that the student is eligible for the course they want to study. While each bank may have slight differences, most follow the same general criteria. Meeting these requirements increases your chances of loan approval and makes the process faster.

1. For the Student Applicant

- Citizenship: You must be a Nepalese citizen to apply for a Nepal-based education loan

- Age: Usually 18 years or older. For bachelor’s or diploma courses, the upper limit is around 35, and for master’s courses, it can go up to 40.

- Academics: You should have completed 10+2 or higher studies, often with minimum marks like 60% or more. Good academic performance strengthens your application.

- Admission: You need a confirmed admission offer from a recognized institution for an eligible course, whether in Nepal or abroad.

2. For the Co-applicant (Parent/Guardian/Relative)

- Income: Must have a steady and verifiable income through salary, business, or rental.

- Income Stability: Banks check if the income can cover the loan interest during the moratorium period.

- Creditworthiness: A good credit history or score helps with loan approval.

3. Loan Specifics

- Collateral: Some loans require property, fixed deposits, or other assets as security, depending on the loan amount.

- Documents: Banks will ask for ID, citizenship, academic records, admission letters, income proof, and collateral papers if applicable.

Banks like Nabil, NIC Asia, Sanima, and others may have slight variations, so always check the specific requirements before applying. Understanding these criteria helps you prepare in advance and avoid delays.

Which Countries Require Education Loans for Nepali Students?

Nepali students typically need education loans to study in countries with high tuition and living costs, such as Australia, the United Kingdom, Canada, the USA, South Korea, France, and New Zealand. These loans help cover tuition fees, accommodation, travel, health insurance, and other study-related expenses that families may find difficult to pay upfront. By taking an education loan, students can pursue quality programs abroad without compromising on opportunities or putting a strain on family savings. Understanding the specific loan requirements for each country ensures students can plan effectively and choose the best programs for their academic and career goals.

1. Australia

Students who wish to study in Australia often face high tuition fees and living costs, making an education loan necessary. The loan can cover tuition, accommodation, food, health insurance (OSHC), and travel expenses. Banks usually require proof of admission from an Australian university and a co-applicant to secure the loan. With flexible repayment options and moratorium periods, Nepali students can focus on their studies in Australia without financial stress. Education loans also allow students to preserve family savings while pursuing world-class programs.

2. United Kingdom (UK)

An education loan is important for students planning to study in the UK, where tuition and living costs are high, especially in cities like London. Loans typically cover tuition, accommodation, visa fees, travel, and day-to-day expenses. Students need to provide an admission letter and often collateral, depending on the loan amount. With proper loan planning, Nepali students can choose top universities in the UK based on merit rather than affordability. This financial support ensures they can fully focus on academic success while studying in the UK.

3. Canada

Students wanting to study in Canada require loans because international tuition and living costs can be high. Education loans cover tuition, accommodation, food, health insurance, travel, and study materials. Banks may ask for a co-applicant and financial proof to approve the loan. With these loans, Nepali students can pursue quality programs in Canada without compromising on opportunities. Loans also allow families to maintain financial stability while supporting their child’s overseas education.

4. United States (USA)

Nepali students who plan to study in the USA need education loans due to the high tuition for undergraduate and postgraduate programs. Loans cover tuition, accommodation, travel, health insurance, books, and other necessary expenses. Banks typically require admission documents like an I-20 form and a co-applicant with proof of income. Education loans make it easier for students to choose programs based on interest and career goals rather than cost. This financial support ensures they can fully focus on academics while studying in the USA.

5. South Korea

Students aiming to study in South Korea may need loans to manage tuition and living expenses for international programs. Education loans cover tuition, dorm fees, insurance, travel, and daily living costs. Banks require admission letters and a co-applicant’s financial documents for approval. With a loan, Nepali students can take advantage of specialized programs and scholarships in South Korea. Loans also provide flexibility in repayment, allowing students to settle financially after completing their course.

6. France

Nepali students who want to study in France often need education loans because, while tuition can be lower, living costs in cities like Paris are high. Loans typically cover tuition, accommodation, food, travel, and insurance. Banks may ask for proof of admission and co-applicant financial documents to secure the loan. Education loans help students focus on academic performance while living in France without financial pressure. They also allow families to support education without exhausting savings.

7. Other Countries (New Zealand, Germany, Japan, etc.)

For students planning to study in New Zealand, Germany, Japan, or other countries, education loans are often necessary to manage tuition and living costs. Loans can cover tuition fees, accommodation, travel, health insurance, and study materials. Banks usually require admission confirmation and a co-applicant with financial proof. With an education loan, Nepali students can explore global programs without compromising on quality or opportunities. Loans also provide flexibility, ensuring repayment is manageable after graduation.

Benefits of Taking an Education Loan Through SAS Education Consultancy

Getting an education loan can be confusing, especially if you are planning to study abroad. SAS Education Consultancy helps make the process simple and smooth. They guide you step by step, from choosing the right bank to submitting documents and getting approval. Using their services can save you time, reduce stress, and improve your chances of getting the loan.

1. Expert Loan Guidance

SAS Education Consultancy provides clear guidance on all types of education loans. They help you understand interest rates, repayment options, and which bank suits your needs best. If you are planning to study abroad, they explain country-specific requirements and costs. This ensures you make the right choice without confusion or mistakes.

2. Bank Coordination Support

The consultancy communicates directly with banks on your behalf. They help you submit applications correctly and follow up with the bank for faster processing. This reduces delays and ensures your documents are complete. You don’t have to visit multiple banks or deal with complicated procedures alone.

3. Study Abroad Counseling Integration

SAS Education Consultancy combines loan support with study abroad counseling. They advise on university selection, admission process, visa requirements, and course eligibility. This way, your education loan and study plans are aligned perfectly. You get a complete solution, not just a loan.

4. Higher Approval Chances

With expert guidance and complete documentation, your loan approval chances increase significantly. Banks are more likely to approve applications that are well-prepared and accurate. The consultancy helps you avoid common mistakes that can cause rejection. This makes your journey to higher education smooth and stress-free.

Conclusion

An education loan is a bridge that turns educational dreams into reality, whether in Nepal or abroad. By providing access to tuition, living costs, travel, and other study-related expenses, education loans empower students to pursue quality programs without compromising their future. Choosing the right bank, understanding interest rates, preparing complete documents, and following eligibility criteria are key to a smooth approval process.

Looking to study abroad? SAS Education Consultancy can help you secure the best education loans, guide you through admissions, and provide top IELTS classes to boost your chances of success. With expert guidance, students can navigate complex procedures, select the most suitable loan, and focus on their studies confidently. Ultimately, an education loan is an investment in knowledge and career growth that opens doors to global opportunities.